2024 Portfolio Review

01 Jan 2025 . Category:

Portfolio

PortfolioReview

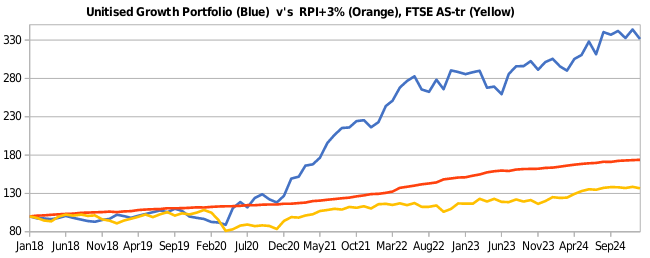

Performance this year has been mixed with an increase of +8.5%, ahead of myRPI+3% (+6%) benchmark but just trailing the FTSEAS-TR

(9.2%).

Portfolio

The portfolio has an anti-ESG bias, trying to take advantage of mis-pricing caused by ESG constraints eg funds not allowed to own tobacco/coal, transition to electric will be slower than thought (oil will be needed much longer), coal still essential and growing etc. There is also a bias to inflation beneficiaries - asset light, real assets etc.

Consumer Staples

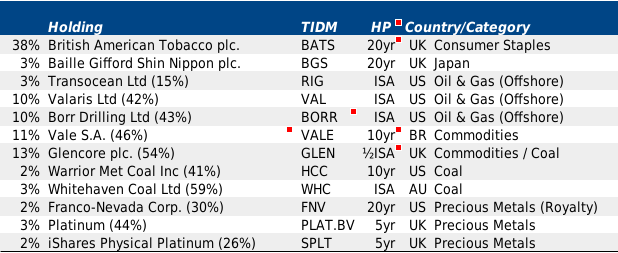

My largest position remains BATS, which provides good income and is an asset light, non cyclical. I’ve noted that at times it does appear to be uncorrelated to the market, which I like from a portfolio perspective (bond substitute). The price fell significantly during the year but I averaged down in the £22-23 area, creating a very unbalanced portfolio. I sold about a third in the £28-29 area and have the significant dividends on top. I may trim this further but will keep a high overweight as I think it provides me with a safe income stream with unrecognised growth catalysts (Vapes+oral, EM exposure, call option on weed). BATS are managing their debt “maturity wall” well, once it becomes apparent it’s a non-issue I’d expect a re-rate (catalyst could be increased buybacks).

Following Nick Train, I initiated a Diageo position - which kept falling. This gave some premium Brands exposure, choosing this as I was less keen on other options such as Unilever. I subsequently sold the position to crystallise a loss, I was unconvinced on the inflation protection of DGE’s premium brands and the market gave better opportunities elsewhere.

Oil and Gas

Oil and Gas exposure is via offshore drillers (“Steel on water”) which should be long term beneficiaries of structural inflation and my energy theme. These shares trade at 2022 levels, at a fraction of book value. I think they give better inflation protection than regular oil and gas companies and with significantly less political risk. The industry is consolidating, which should lead to pricing power for the scarce assets with high barriers to entry.

They have fallen significantly and I’ve averaged down making them large holdings. These are highly cyclical, with the ability to multibag and then lose it again quickly. I expect this cycle’s performance may exceed that of the last: offshore is one of the cheapest options for oil companies, the theory is that there will be a shortage of rigs. It takes years to build a new rig/drillship, less credit may be available this time around (burned last cycle) - day rates should move up and to companies turn into profit making buyback machines.

Borr Drilling gives exposure to Jackups. Some of the recent negative price action may be explained from them de-listing in Oslo, with Norwegian pensions / sovereign wealth unable to hold. Transocean is a high debt company focused on semi-subs/drillships, this could give the best return but at a high risk (in an inflationary environment the debt becomes an asset). Valaris is in the same segment as Transocean, but with little debt after coming out of bankruptcy.

Coal

The narrative on coal is that it is being phased out and replaced with green alternatives. However, a recent IEA report paints a different picture, noting that 2024 coal demand was at a record high and now sees higher demand in 25, 26, 27. Never mind peak oil, we haven’t even hit peak coal!

My coal exposure is via Whitehaven, Warrior and Glencore, which includes both Thermal and Coking coal. Both Whitehaven and Glencore have completed significant coal transactions, and I think that as these are digested and the cashflow appears, we could see a re-rate of the shares. The catalyst for Warrior Met Coal is that it’s building a new mine which should come online shortly.

I’ve also been looking at Alpha Metallurgical Resources, and may switch some offshore money into that to reduce overweight offshore risk.

Commodities

My commodity exposure is through Vale and Glencore. I split the (~40%) coal out of the Glencore holding and count that under the coal weighting for better visibility.

My emphasis is on the bulks which, although isn’t sexy, is apparently where the money is made. Near term Iron Ore demand looks suspect, but I’m hoping this is priced in. Iron ore is a proxy for world growth (infrastructure, buildings, etc) and I think it should be OK, especially if there is any stimulus.

My Vale holding grew too large as I averaged down, I’ve since crystallised losses and moved into offshore to diversify. It’s very cheap, and I was expecting a bounce now the new CEO has been appointed and that the damages for the dam collapse decided. As a huge % constituent in the Brazil market, I believe it has been driven down further due to the sell off there. I’m stopped out of buying more due to 30 day rule, probably a good thing.

Glencore gives me exposure to Coal and Copper. They also get a significant amount of revenue from a trading business, which will act as an internal hedge as it should make money in both raising and falling markets. Glencore recently bought Teck’s coal business, and I’m expecting a significant increase in profits from them. I like Glencore’s approach - unlike their peers, they are happy to invest in coal rather than pander to the ESG movement.

A purchase of Trident Royalties resulted in a 20% gain, following their takeover by an Australian royalty company.

I sold my investment in Ecora Resources for a large loss. It was a bad investment, the most ESG of my holdings (battery metals) didn’t fit with my theme. The share price performance reflected the 2024 acquisitions of battery metal royalties on mines which now look like they may not get built following the crash in the Nickel price. Ecora may suffer from EV take-up slowdown and may be have issues once their coal royalty comes to an end (Ironic that the ‘woke’ company is relying on coal). I moved the sale proceeds into Glencore as I prefer their coal/copper mix, more of a sure thing (not betting on battery Chemistries).

Precious Metals

A huge position in Adriatic Metals was sold prior to the expected re-rate, for a 30%-ish gain. The share often moved before official announcements, the CFO resigned and so I decided to cut my gains. Subsequently the CEO resigned and the price crashed, but since recovered. Going forward, I am going to avoid smaller miners as think larger companies offer better risk reward.

There were also successful trades in the PGM miner, Sibanye Stillwater. I decided that I didn’t have to make my ECOR losses back the same way I lost them, so bought SBSW in low/mid 4’s and sold at high 5’s. However, I was uncomfortable with the holding (debt) and sold to buy PGMs directly.

I initiated a significant position in Platinum. The metal has traded above gold in the past but is now substantially cheaper, it would have to 2.5x to get back to that level. The asymmetric risk reward looks good, with maybe 20% downside or so. It has suffered from expected lack of demand due to EVs, but this now appears to be in doubt as many manufacturers pulling back from EVs and instead looking at hybrids which have high PGM loadings. Platinum also has other ‘green’ growth uses such as hydrogen fuel cells. I’ve read that many jewellers are stocking more platinum as the working capital required is much less than holding a large stock of gold jewellery. Platinum is a veblen good, a higher price makes it more sought after, increasing demand (like luxury handbags).

Taking the advice “You rarely get an opportunity to buy a quality company at a discounted price”, I initiated a small position in Franco Nevada. A levered play on gold with better inflation protection than the miners. It has fallen a lot due to the closure of one of its main mines in Panama, but there is speculation it could re-open. Either way, with central banks buying gold (following Russian reserve confiscation), I think the share has good prospects.

Japan

Japan is one of the worlds cheapest markets, and I was keen to get exposure to the small cap deep value theme using AJOT. But that raced away from me and so I decided that BG Shin Nippon at a 16% discount and near multi year lows was a good alternative. Japan Small Cap deep value has had good performance and I think some of this has been at the expense of small cap growth, which I hope will mean revert. Long term, I still prefer the value theme and so may switch should the opportunity arise.

Comment

Performance up until November was good, well ahead of benchmarks, but then experienced a rapid drop off in December. I think it’s has likely suffered due to end of year tax loss selling.

Full year performance has been saved by my overweight BATS position, which has cushioned the losses elsewhere. I have used this as a funding source to top up elsewhere.

My intention is not to follow the crowd, and avoid overvalued areas of the market - specifically tech dominated US markets. It is psychologically uncomfortable to go against the crowd and buy unloved sectors that keep falling. My position sizes are too large, yet I find it difficult to diversify into other areas where I’m less keen on the outlook. I think Buffett(?) talked about 50% of portfolio in your best idea, 10th idea not as good as 1st, etc.

No real insight into what 2025 has in store, only that my investment ideas have some rationale to suggest growth in the medium term. I had hundreds of trades this year, which I think did add value - I plan to trade less going forward as I am keen to minimise tax the consequences.

Iain Benson is a real person and not a grassy plant viking. He lives in Scotland. In his spare time, Iain likes tinkering with his Raspberry Pi, going for long walks and drinking wine. Preferably all at the same time.