2025 Portfolio Review

01 Jan 2026 . Category:

Portfolio

PortfolioReview

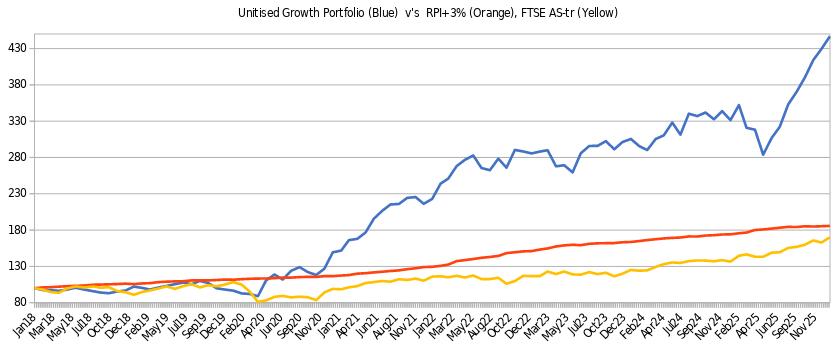

Overall, a solid performance this year with an increase of +34.8%. This is well ahead of both RPI+3% (+6.7%) and the FTSE All Share Total Return (+24.4%) benchmarks.

Portfolio

Current holdings:

The portfolio aims to provide inflation protection with exposure to asset light companies, commodities and precious metals. There is an anti-ESG bias, trying to take advantage of mis-pricings caused by ESG constraints eg funds not allowed to own tobacco/coal, transition to electric will be slower than thought (oil will be needed much longer), coal still essential and growing etc.

Nicotine

Last years largest position was BATS at a 38% weighting. The price of the Stock ran up to around £44, and I started reducing in the late £30’s up to £44. This held up very well in the April sell off, and was used as a source of liquidity. Over the last 5 years, total return has been around +37%. I still like the thesis, and the dividend, though there is better value elsewhere, and so the opportunity to switch was taken (mainly into Glencore). The small residual holding will likely be sold.

Premium Alcohol

The idea behind the premium alcohol thesis is that people are drinking less, but when they do drink they want better quality. I read that drink sales form a power law distribution - the top decile (or 2) of people do the bulk the drinking, they may be less likely to worry about health etc.

Investments were made in Diageo at a 12 year low (down over 50%) and also Rémy Cointreau at an 18 year low (down 80%). These have sold off as investors worry that drinking is less popular due to weight loss drugs / healthier lifestyles. I’ve taken the opposite view as see alcohol consumption as lindy, and invested in these quality businesses while trading cheaply.

“You’re paying single-digit to low-teens multiples for global habits that have survived wars, recessions, and moral panics”

Diageo offers broad exposure to spirits and also owns Guinness which is selling well, it could be a takeover target at current levels. A new CEO is starting in January and so the turnaround might be imminent.

Rémy is focused on cognac, this post discussed how it is likely trading below book value as the value of maturing cognac inventories are understated (and that value goes up the older it gets). The ageing stock forms a deep moat, no competitor can suddenly create 50yr matured cognac. The business has high margins, a luxury type business which should exhibit pricing power inelasticity (somewhat recession proof).

Oil and Gas

Oil and Gas exposure is via Offshore drillers. The thesis is that that they trade at a fraction of replacement cost; it takes years to build a new rig/drillship and they are in limited supply. Once the new offshore cycle starts the dayrates should increase significantly, the rates are currently far far below those required to incentivise new builds. Teir 1 shale oil development in America appears to be slowing and offshore the cheapest new oil available to oil companies.

“the secret is to look for consolidating industries and avoid highly competitive/fragmented industries”

This sector is consolidating, leading to pricing power for scarce assets with high barriers to entry. In inflationary times, scarce assets are exactly what we should be holding.

As the price of oil increases, many oil companies may face populist windfall taxes - offshore services are a clever way to participate in an oil rise but avoid this political risk. A picks and shovels play.

But there is a downside! This sector is highly volatile and cyclical. In the April sell off, the holdings lost over 50% in value. Top ups were made by selling holdings that had gone down less, making this risky sector an overweight. This gamble paid off as many holdings are up over 100% off the lows. This has been a major driver of this year’s portfolio return.

Transocean is the principle holding, giving exposure to best in class semisubs/drillships. It has significant debt and so most levered to the thesis. In inflationary times, it is said that debt becomes an asset (as gets inflated away). Many consider this a poor sector pick, but it has most contracted book compared to competitors - Mohnish Pabrai noted this lack of white space hints to quality of ships, crew and business acumen compared to the other players. By avoiding bankruptcy in the last cycle, it kept hold of experienced employees. As the best known driller, it should benefit from fund flows if there is a retail push into the sector.

A holding in Noble is maintained as some sector diversification. They appear to be well managed. Valaris was sold after a 100% gain off the lows, I’m not convinced about their management and the lack of buybacks at the lows, despite being ‘cashed up’ (and buying much higher).

The portfolio retains a significant holding to BORR Drilling which operates a fleet of modern jackups. This share has faced it’s own idiosyncratic issues and is down a lot, but these appear to be resolving and it’s prospects look good going forwards.

I initiated a position in the North Sea based Harbour Energy. While I’m cautious on governments levying windfall taxes on oil companies, I don’t think those Harbour face could get much worse than 78%. Indeed, could view this as a play on the government eventually easing up on the tax regime once it become apparent they’re destroying UK oil industry/receiving less revenue. This position was reduced following the announcement they would takeover LLOG, which would mean much more debt and so the risk reward changed (took ~5% loss).

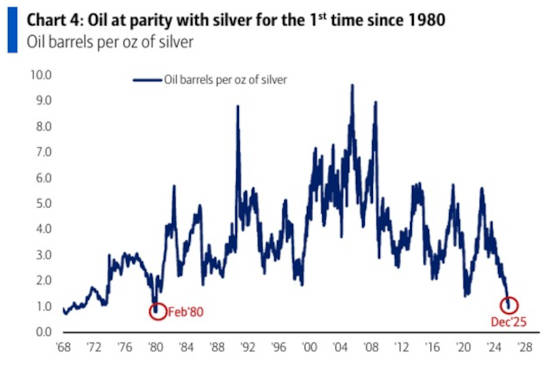

The oil price seems to be at a generational low when compared to that of real money. The chart below shows barrels per Oz of silver. In inflationary environments Precious Metals are said to move first with other commodities later.

Commodities

Commodity exposure is via generalist large cap companies that will benefit from my commodity cycle theme. My emphasis is on the bulks which, based on past cycles, is where the money is made. When compared to the S&P around all time highs, prices could be viewed as cheap. After years of underinvestment, all the conditions are present to foment a bubble. Following the precious metals breaking higher, I suspect that the trend will push out into industrial metals.

“Soon, all commodity charts will look like gold”, Bank of America’s Hartnett

This post talks of how the U.S. is no longer claiming global leadership, but is retreating to its own hemisphere. Re-industrialisation is now thought to be a US top priority (factories/mines/supply chains) as without strong production base there is no military might. Recent actions in Venezuela and the rush to secure critical minerals would appear to confirm this “hemispheric dominance” strategy. This re-industrialisation will require physical commodities which could result in decades long commodity boom in this new era of hemispheric competition. Interesting.

Iron Ore prices have remained suppressed through the year. The Vale holding was reduced as the lack of double tax agreement between the UK and Brazil meant paying tax twice. I diversified into Labrador Iron Ore Royalty Corp, a Canadian ‘compounder’ , with the royalty structure giving additional inflation protection. I’m not super bullish, as Iron ore can be viewed as a proxy for world growth.

Glencore gives exposure to Copper and Coal, along with their trading arm (uncorrelated returns?). Copper is THE energy transition metal, battery chemistries change but the requirement for copper won’t. Key points: several large mines have gone offline this year, ore grades have collapsed from ~2% to <1%, few new discoveries and takes ~20yrs to go from discovery to production. In other words, supply is tight (falling 1.5%/yr) while demand keeps rising (1.6%/yr) - this indicates higher prices going forward. Holding GLEN also gives a call option on the possibility of a merger with RIO. In short, Glencore gives multiple ways to win.

S32 was purchased to diversify the Glencore holding. These are ex BHP assets. It gives exposure to aluminium, where destocking is taking place and US premiums are at highs. In the US there appears to be competition between aluminium refiners and AI data centres for power. Aluminium could also benefit from from copper substitution. S32 also gives exposure to silver and ‘critical minerals’ which aren’t in the price, with the recent silver price rise this could be a significant.

Coal

The coal allocation is weighted towards thermal, direct met coal holdings were sold with Glencore now providing that exposure.

Thermal coal is a capital starved sector, with major producers pulling out. It gives an opportunity to play the AI bubble indirectly and cheaply. I like to express views indirectly as often the 2nd derivative doesn’t reflect reality (until it does). The power demands of AI data centres mean that coal (and gas, though lead times on gas turbines are ~6yrs) will likely fuel most of that demand as they are the only reliable sources that can quickly ramp up. This comes at a time when investments in coal and gas production have been weak.

That said, AI is only a fraction of global coal demand. In the coming years, 7 billion people in developing markets will vastly increase their energy usage to reach the same living standards as the West. Electricity production in the developing world is dominated by coal. I read that India has said it could now continue building coal plants until 2047, resulting in a 87% increase in coal power capacity from 2025.

In short, supply growth is constrained and demand will continue to grow which creates a compelling opportunity.

Coal is represented in the portfolio via Glencore and Thungela. Thungela is a spin off from Anglo American who divested their coal portfolio. It’s down over 80% from it’s recent high. If I had to bet on a company that could 10x, it’d be this.

Chemicals

I initiated positions in chemical companies Dow and LyondellBassell. Most of my investments have a catalyst which I expect to drive returns, the investment here was based on the fact they are a key sector and have fallen so much that they must rebound.

China is said to have saturated the chemicals market, but could an East/West bifurcation (see below) be the catalyst to re-rate the price of the chemical stocks? Regardless, these companies pay a good dividend while I wait for them to be re-rated or for the world to end.

Precious Metals

Performance has been spectacular with the direct Platinum holdings up 110% this year. The main mistake of last year was not weighting this sector more heavily as it was an obvious trade. It should have been a 10+% position.

Franco Nevada was sold for a 1 yr gain of 21% and moved into palladium/platinum prior to their run.

Many might suggest that the sensible course of action would be to exit after this strong run, but I continue to hold as think the outperformance could continue.

One of the reasons for investing heavily into platinum was that the gold price had increased, and platinum had not moved. This has played out as expected, but still needs to more than double to match gold’s price (remember it used to be more expensive than gold!). I expect another 100% gain in platinum from here, probably more as I think gold will keep rising with 2 major drivers : devaluation & de-dollarisation (central banks). When compared to money supply, gold could still be considered cheap, even after this year’s 48% increase.

2/3rds of the physical platinum was sold on the Oct pull back and moved into the miner Valterra Platinum. This continues the profitable game of buying deeply discounted assets that were sold off by Anglo American. Valterra should give levered exposure to the platinum price and pay a dividend (instead of having to pay a carry cost). It also gives significant exposure to Palladium/Rhodium, and has the longest life mines in the sector. Retaining some physical platinum serves as a natural hedge: if there is an issue with Valterra then the platinum price would re-rate higher and offset the loss.

Tensions with China are rising: China implementing export controls on rare earths/silver, US banning chip sales and seizing Venezuelan oil tankers

bound for China (squeezing them out of Latam oil and metals?). Could this signal a bifurcation between East/West (see hemispheric dominance above)?

We could be viewing the re-monetisation of Gold prior to the return to a multipolar world - in which case this could be the new normal, rather

than a price spike. Not adding here, but very happy to continue to hold.

Japan

Japan positions were closed and moved to oil, which I think has better prospects in next 1-2 years.

Transportation

I initiated holdings in shipping and rail companies, all at low valuations.

Rail companies operate as pseudo monopolies with high replacement cost. They are the lowest cost of on land transport and can be viewed as ‘green’. I bought into Canadian National Railway, other owners include Bill Gates (it was his largest position) and Personal Assets Trust (a fund I rate highly). Long term hold.

In shipping investments were made into Clarkson (an ‘asset light’ ship broker) and Star Bulk Carriers (A ‘drybulk’ carrier). The drybulk thesis is that a decade ago there was an over supply of ships and so in recent times there have been few new vessels built. Supply: Towards the end of the decade ~1/3rd fleet will have to be retired since they’re older than 20yrs (Clients prefer newer ships, insurance becomes difficult) with not enough replacement vessels to fill the gap. Demand: New Iron Ore Mine in Guinea with China looking to diversify (new route 3x distance of old routes). Demand up / Supply down = opportunity. Star Bulk has a range of vessel types, it’s been described as the closest thing to a drybulk ETF.

Global Exchanges

Exchanges are an asset light contra-cyclical and can be thought of as operating a quasi-monopolies, providing essential economic infrastructure. When stocks crash, exchange volumes increase and these companies earn more money. Neat portfolio hedge.

The London Stock Exchange was added following a 30% fall, trading at it’s lowest P/CF in 10 years. I added the Australian ASX which is a more commodity focused exchange, again around 30% from highs. Horizon Kinetic’s 3Q25 report noted that the performance of exchanges has exceeded that of their respective stock indices, and by some margin. The report noted that the exchanges don’t correlate with each other so there is a case for holding a basket of them. I expect to add further exchanges in future.

Commentary

This year the portfolio significantly outperformed the benchmarks and marked the 6th year of positive returns (55%, 49%, 28%, 7%, 8%, 35%). As I hope I have demonstrated above, most of the themes have catalysts in place to suggest that the performance could continue in the coming years.

In the April sell off, the portfolio was down over 20% which was quite uncomfortable. Since then the turn around has been impressive, on the chart it looks somewhat unnatural with 8 months of consecutive new highs.

The portfolio has a clear bias towards consolidating industries/monopolies, this allows them to exert significant control of the market and charge higher prices than would otherwise be possible. There is also a significant weighting to capex heavy businesses (oil, coal and commodities) which account for over a 60% weighting. With that in mind, the following observation was interesting:

I’m gonna say it again since we’re in a generational economic shift:

What if capex heavy businesses are automatically moated moving forward?

Who is going to compete for less than 15% ROIC?

Many capex heavy businesses will achieve excess returns over next decade.

Companies like VALE, GLEN, RIG, BORR have large sunk costs, with the cost to replicate in an inflationary environment only increasing. An ever increasing moat. Or, as SomeGuy™ on twitter succinctly said:

Buying scarce tangible assets using yesterday’s dollars leads to high pricing power and inflation only increases the capital barriers to entry

Most portfolio holdings are down between 30 to 80% from their all time highs. I don’t view them as expensive. I do view the wider SP500 as expensive as the overweighted MAG7 continue to push the market higher. With a few exceptions, my holdings lie on the other side of the ‘ETF divide’, that is the shares aren’t in and haven’t been subject to ETF flows. That’s going to be important moving forward.

To be clear, short term the prices could drop significantly as commodities are volatile. I hope to lighten up as the commodities bull progresses, though it will be difficult to know when to sell.

I executed ~450 trades this year, a huge number. Thousands of pounds in fees. Every year I state that I’ll trade less, but I now hope my portfolio can remain more static in 2026. The eventual aim is to end up with a portfolio of never sell companies which is more tax efficient.

Following gold’s rise, I think 2026 could be a very good year for commodities. The portfolio in now not very defensive, so could suffer significantly in the event of a recession. I’m hoping that the low valuations will provide some protection in the event of a downturn.

Iain Benson is a real person and not a grassy plant viking. He lives in Scotland. In his spare time, Iain likes tinkering with his Raspberry Pi, going for long walks and drinking wine. Preferably all at the same time.